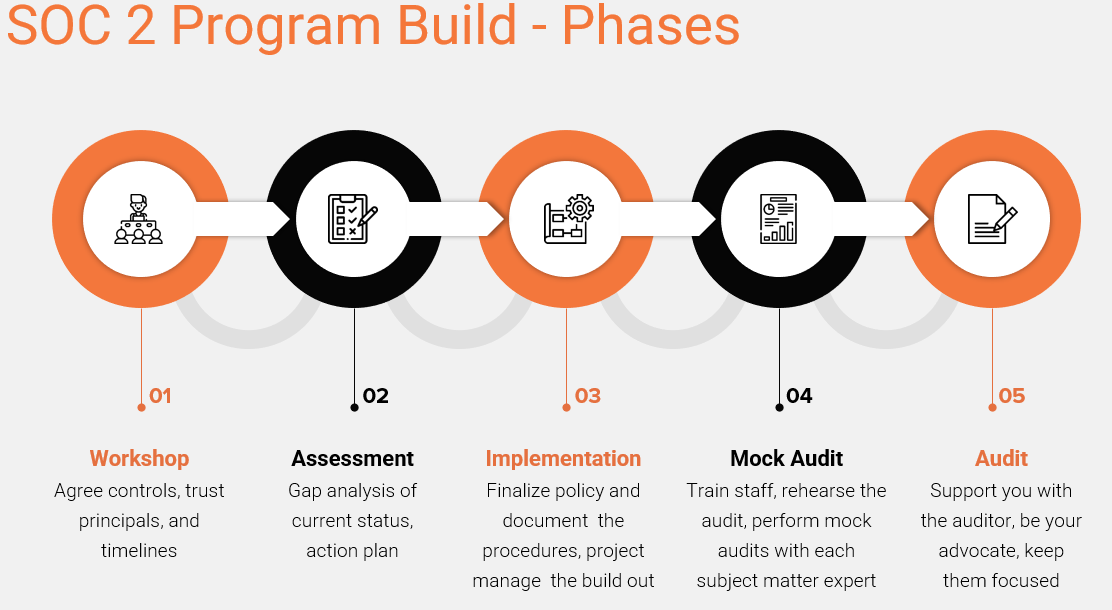

The SOC 2 or 'SOC for Service Organizations' report evaluates controls relevant to maintaining the data management system's security, privacy, confidentiality, availability, and processing integrity. It is intended for use in response to governance, risk and compliance inquiries, executive management oversight, and demonstrative due diligence. There is considerable flexibility for customization in the SOC 2 framework, and report formats vary across auditors and organizations. The report is typically segmented into five sections, each with its distinct responsibilities.

Section One: Independent Service Auditors Report - Auditor (CPA)

The independent auditor's report is the summary opinion of the CPA performing the audit. This section describes the scope of the auditor's examination, the auditor's responsibilities, a description of the system under review, the relevant Trust Services Criteria, and the auditor's overall opinion as to the effectiveness of the controls given the business objectives. If the report is a type 2 audit, the auditor will also describe the period, testing methodology, and summary results.

The auditor may also describe things not tested. For example, the scope of the audit may not include an examination of the multi-factor authentication solution. In this case, the auditor will state their assumption that the MFA solution is sufficient to satisfy the TSC or the user entity controls requirements.

Section Two: Management's Assertion - Organization

This section contains the facts and assertions made by management regarding the suitability of the information management system controls. The management's assertion section summarizes the system under audit, TSCs used subservice organizations, CSOCs and CUECs, and the exam period. Management confirms why based on their best knowledge, the controls in place are suitable to meet the business's service commitments and system requirements.

Section Three: Description of the System Under Audit - Organization

The system description section renders details of the system, including scope, boundaries, controls, and related contractual and statutory commitments. In addition, it includes the services the organization provides and its primary obligations and requirements.

This section may also contain management philosophy of relevant aspects of the control environment, including security policies and management, personnel and physical security, change management, monitoring, disaster recovery, and risk assessment.

System Elements:

Infrastructure describes the hardware platform infrastructure. For example, infrastructure could talk about the number and types of servers running and their physical location, networked, and employee access points such as VPN gateways.

This subsection talks about the chain of software used by the information management system from the OS to off-the-shelf and proprietary software and user interfaces such as web apps, APIs, and communication stacks.

This section describes all the organization's employees, their job functions, and how they interact with the information management system. The people section also describes any utilized system monitoring and metrics, documentation, and training programs.

This section describes critical procedures related to managing the information system. The procedures section can include detailed methods for data classification, system monitoring, maintenance, and incident response.

Data the data section includes customer data, transaction data, reports, system files, and error logs.

This subsection details any cyber-attacks or other system incidents suffered during the examination period. In addition, it includes details of the incident(s), the organization's response, and mitigating control changes put into operation.

Section Four: Auditor's Tests of Controls (type 2 only) – Auditor (CPA)

In the introduction of this section, the auditor details TSCs relevant to the report and defines their meaning concerning the information system at hand. The body of this document section is typically a four-column table summarizing:

- The control criteria objective

- The relevant organization control in place

- The auditor's test of the control

- Result

Auditor's Test of Controls Example Entry:

| Trust Services Criteria for the Security Category |

Description of Service Organization Controls |

Auditor's Test of Controls |

Result of Tests |

|

CC6.5 The entity discontinues the protection of physical storage devices only after destroying the ability to retrieve data from those devices.

|

Formal device disposal procedures are in place.

|

Inspected device disposal procedures to determine they were in place.

|

No exceptions noted.

|

|

Before removal from the facility, all storage devices are degaussed and sanitized.

|

I examined a sample of destroyed media to determine that sanitization measures are applied.

|

No exceptions noted.

|

'No exceptions noted' is the best grade you can get on SOC 2 reports. One or more exceptions do not necessarily degrade the overall opinion of the report. Instead, the auditor will root cause the exception and consider whether the system continued to meet its service commitments and requirements.

Section Fives: Unaudited Information

No exceptions noted' is the best grade you can get on SOC 2 reports. One or more exceptions do not necessarily degrade the overall opinion of the report. Instead, the auditor will root cause the exception and consider whether the system continued to meet its service commitments and requirements.

Section five is open for any additional relevant information management wants to add to the report. Typical use is for management response to exceptions.

Common Criteria, CSOCs and CUECs

Complementary subservice organization controls (CSOCs). These are controls that must be in place by a subservice provider for the organization under audit to meet its TSC objectives. For example, an organization that uses a data center colocation service may require that the service provider provide physical security with restricted access controls and environmental monitoring with fire suppression capability.

Complementary user entity controls (CUECs) are necessary controls combined with the service organization's controls to meet the stated control objectives. For example, requiring employees to use smart cards for physical access and strong authentication to log in are CUECs.

The SOC 2 Trust Services Criteria (TSC) and example controls

- Security

- Firewalls

- Intrusion detection

- MFA

- Availability

- Performance monitors

- Backup and disaster recovery

- Incident Response

- Confidentiality

- Strong Encryption

- Access controls

- Privacy

- Access monitoring

- MFA

- Strong Encryption

.png) Are you considering a security program for your organization? We work with clients just like you to implement a modern and reliable security program. Read our security program guide to learn what goes into a security program, who needs to be involved, and more to ensure long-term success.Learn More

Are you considering a security program for your organization? We work with clients just like you to implement a modern and reliable security program. Read our security program guide to learn what goes into a security program, who needs to be involved, and more to ensure long-term success.Learn More